Environmental Obligation Management Is a Governed Workflow

Environmental Obligations are not managed through isolated activities or point-in-time decisions. They are governed through a defined, repeatable workflow that persists for as long as an obligation exists. This workflow is the mechanism through which enterprises control, defend, and ultimately resolve Asset Retirement Obligations (ASC 410-20) and Environmental Remediation Obligations (ASC 410-30).

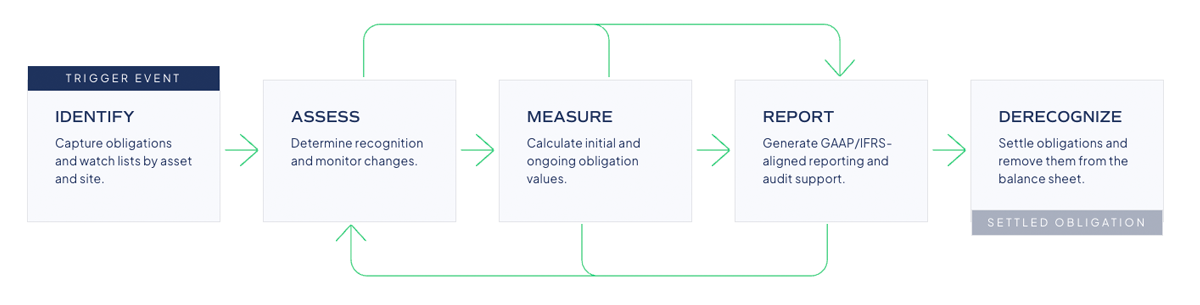

In Environmental Obligation Management, governance does not occur at a single moment. It is enforced across a lifecycle consisting of five distinct stages:

Identify → Assess → Measure → Report → Derecognize

These stages are not optional and they are not linear checkboxes. Together, they form a governed lifecycle that determines whether Environmental Obligations remain controlled and defensible over time, or devolve into audit risk, unexplained variance, and value leakage.

EXPLORE ENFOS TODAY

Identify: Where Environmental Obligations Enter the Workflow

Identification is the point at which Environmental Obligations are introduced into the governed EOM workflow. Triggering events include asset acquisitions, facility construction, contamination discoveries, regulatory actions, and asset retirement planning. These events can originate anywhere in the enterprise.

Identification is therefore a control activity, not an operational task. If Environmental Obligations are not consistently identified, they never enter governance. Obligations that remain unidentified cannot be assessed, measured, reported, or managed, creating latent business risk.

Assess: Where Obligations Are Characterized

Assessment determines whether an identified condition gives rise to an Environmental Obligation and how that obligation should be characterized. This stage relies on scientific evidence, regulatory interpretation, and legal context to determine scope, probability, and timing.

Assessment establishes the basis for recognition and defines the assumptions that will carry forward into measurement. If assessment is informal or undocumented, downstream financial reporting rests on weak foundations. Governance failures at this stage propagate through the rest of the lifecycle.

Measure and Report: Where Business Risk Is Managed Over Time

Measurement and Reporting form the ongoing operating rhythm of Environmental Obligation Management. Once recognized, Environmental Obligations do not sit idle between quarters. Assumptions, execution progress, regulatory inputs, and cost profiles must be reassessed and reflected each reporting period. This is where Environmental Obligations continuously surface as ARO and ERO balances and where Finance actively manages business risk through time.

Measurement governs the planned liability. It reflects assumptions about remediation scope, timing, cost, discount rates, and probability, all of which evolve as new information becomes available. Reporting governs how that liability is presented, disclosed, and defended in the Form 10-Q and Form 10-K. Together, these stages ensure that Environmental Obligations remain aligned with reality rather than drifting into static estimates.

This stage requires continuous reconciliation between the planned liability and settlement activity, the actual execution spend applied against specific components of the obligation. Partial settlements accumulate over years before final closure. When settlement activity is not clearly reconciled to the plan, liabilities lose credibility, variance accumulates, and audit risk increases. Surprise accruals and last-minute adjustments are symptoms of governance breakdown at this stage.

Because Measurement and Reporting recur every quarter for as long as an obligation remains on the balance sheet, this is where Environmental Obligation Management becomes an enduring finance function rather than a one-time compliance exercise.

Derecognize: Where Governance Is Concluded

Derecognition is the point at which an Environmental Obligation is removed from the balance sheet. It is not an operational milestone. It is a governance decision that requires confirmation that remediation or retirement work is complete, regulatory requirements are satisfied, legal exposure has ended, and accounting treatment is aligned.

Premature derecognition creates restatement and enforcement risk. Delayed derecognition ties up capital unnecessarily. Effective EOM governance ensures that derecognition occurs only when earned and as soon as appropriate.

EOM: Executive Impact

The EOM workflow is how Environmental Obligations are governed over time. Identification and Assessment define what must be managed. Measurement and Reporting manage risk each quarter. Derecognition concludes governance when obligations are fully resolved.

Environmental Obligations outlive people, systems, and organizational structures, so governance cannot be optional or episodic. If any stage operates outside formal controls, the entire obligation remains exposed. This five-stage Environmental Obligation Management workflow is the foundation for how leading enterprises manage ARO and ERO as enduring financial risk. In the next post, we will map ownership across the workflow and show how accountability is distributed across Finance, Accounting, Operations, Legal, and external stakeholders.

In the next post, we examine why identical facts can still produce different liabilities and how governance and policy shape balance sheet outcomes.