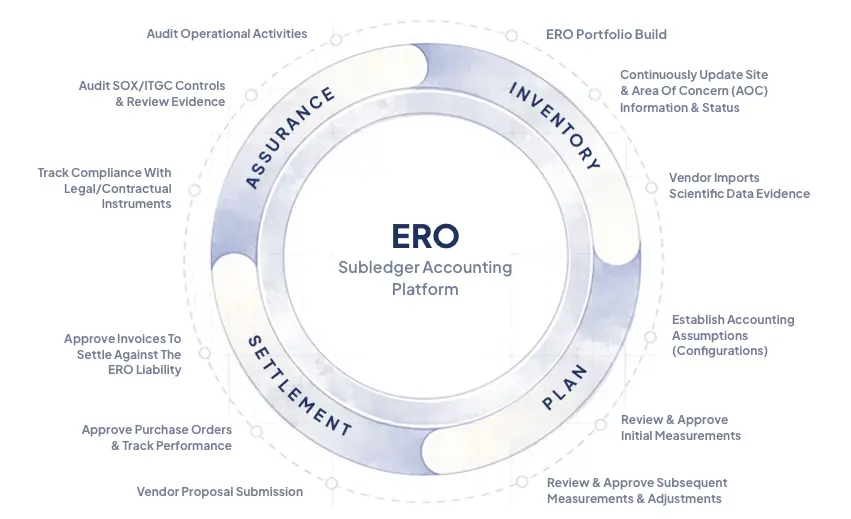

environmental Remediation Obligation (ASC 410-30)

Why spreadsheets fail for managing ERO

What is an Environmental Remediation Obligation?

An Environmental Remediation Obligation (ERO) is a legal obligation to recognize a liability and disclose the future cost to investigate, remediate, monitor, or restore contaminated soil, groundwater, and surface water resulting from past operations, asset ownership, or regulatory action. ERO are recognized and measured under ASC 410-30 when it is probable that a liability has been incurred, and the amount can be reasonably estimated.

Unlike ARO, ERO are typically event-driven, triggered by contamination discovery, regulatory action, asset divestiture, or changes in law, and often involve significant uncertainty, evolving scope, and long-tail settlement timelines.

ERO Scope, Inputs & Attributes

ERO spans across industrial companies with site-specific, event-driven contamination risk, making spreadsheet-based tracking fragile, inconsistent, and indefensible as portfolios scale.

ERO Recognition drivers

Contaminant Concentrations Exceed Regulatory Thresholds

Liability Is Reasonably Estimable

ero spend drivers

Chemicals of Concern

Geology and Hydrogeology

Site Conditions and Demographics

Historical Site Use

Regulatory Standards and Limits

Regulatory Pathway

Planned Future Land Use

Institutional Controls

Remediation Strategy

Cleanup Phasing and Work Breakdown Structure

Legal Mandates (e.g., Consent Decrees)

Property Value

the problem

Environmental Remediation Obligations (ERO) are characterized by uncertain scope, timing, and cost, making liabilities difficult to estimate, account for, defend, and manage toward site closure. They require joint expertise from remediation operations and accounting functions—neither discipline alone can adequately address remediation liabilities. Technical documentation and underlying assumptions are fragmented across consultant reports, scientific data assessments, consent decrees, and regulator correspondence.

Cleanup strategies, assumptions, progress, and closure criteria evolve over time, but changes are not systematically updated or integrated with the accounting framework. As a result, remediation liabilities lack full transparency, information is siloed, and decisions are made reactively rather than deliberately. While the obligation is acknowledged, companies lack a defensible, end-to-end remediation plan that connects the complex technical inputs with the accounting and financial reporting requirements.

the consequences

When ERO are managed across spreadsheets and fragmented systems, complexity arising from cross-domain accountability outpaces control. Manual calculations, fragmented data, and undocumented assumptions undermine financial integrity, increase audit exposure, and create recurring fire drills for the Office of the CFO and Operations.

At scale, spreadsheet-based ERO management is structurally unsound, indefensible, and manual.

scientific data

Disconnected scientific data creates context gaps, reducing historical insight, forecasting accuracy, and remediation decision quality overall.

earnings volatility

Late and incomplete information creates reactive remeasurements, increasing P&L volatility, surprises, and earnings unpredictability over time.

incomplete financials

Disconnected remediation plans create manual processes, reducing reserve accuracy, timeliness, transparency, and close reliability overall enterprise.

Work Breakdown Structure

Unstructured cleanup phasing creates timing distortions, increasing remeasurement noise, forecast variance, and reserve inaccuracy over time.

audit risk

Poor documentation of assumptions creates traceability gaps, reducing audit defensibility, SOX confidence, and regulatory trust overall.

the enfos solution

ENFOS replaces spreadsheets and fragmented systems with a purpose-built ERO system of record for the dual domains of remediation operations and accounting.

The platform centralizes asset inventories, standardizes assumptions, automates remeasurement, and maintains a complete technical and accounting audit trail across the full ERO lifecycle.

By structuring data, enforcing controls, and integrating with ERP and financial systems, ENFOS enables finance teams to manage ERO with confidence, reduce reporting volatility, and withstand audit scrutiny as portfolios scale.

EXPLORE ENFOS TODAY

FAQs

What is an Environmental Remediation Obligation (ERO)?

An Environmental Remediation Obligation (ERO) is a legal or constructive obligation arising from past contamination events that requires an entity to recognize and disclose the estimated costs to investigate and remediate contaminated soil, groundwater, or surface water in accordance with ASC 410-30.

When is an ERO recognized under ASC 410-30?

An ERO must be recognized under ASC 410-30 when environmental contamination creates a probable and reasonably estimable legal obligation to remediate under existing laws or regulatory authority, regardless of whether enforcement has formally begun.

How is an ERO measured and remeasured over time?

ERO is initially measured at the best estimate of expected remediation costs based on current scientific data, regulatory requirements, and available remediation alternatives, and is remeasured each reporting period as new information emerges—such as updated sampling results, regulatory actions, changes in remediation plans, cost inputs, or timing—through adjustments to the accrued liability and expense.

How does ENFOS support audit readiness and internal controls?

ENFOS maintains a complete, system-generated audit trail, including assumption history, roll-forwards, journal entries, and supporting documentation, enabling consistent and defensible reporting.

How does ENFOS onboard customers?

ENFOS onboards customers in alignment with ASC 606, using a structured configuration, data migration, and training process with defined milestones and deliverables designed to support timely platform activation and value realization.

How long does it take to adopt ENFOS ERO Plan Module?

ERO Plan configurations vary by portfolio size and complexity, but ENFOS is designed to onboard enterprise ERO programs efficiently without disrupting close or audit cycles.

How does ENFOS integrate with ERP and financial systems?

ENFOS integrates with ERP and general ledger systems to support journal entry creation, subledger roll-ups, and financial reporting, ensuring alignment between operational data and the GL.