The Governing Mandate

GAAP and IFRS require complete, accurate, and supported measurement and reporting of material liabilities for Asset Retirement Obligations and Environmental Remediation Obligations. Measurement of Environmental Obligations is an executive accountability, not a mechanical accounting exercise. Financial reporting is constructed from these measurements, and executives rely on their integrity to govern material balance-sheet exposure.

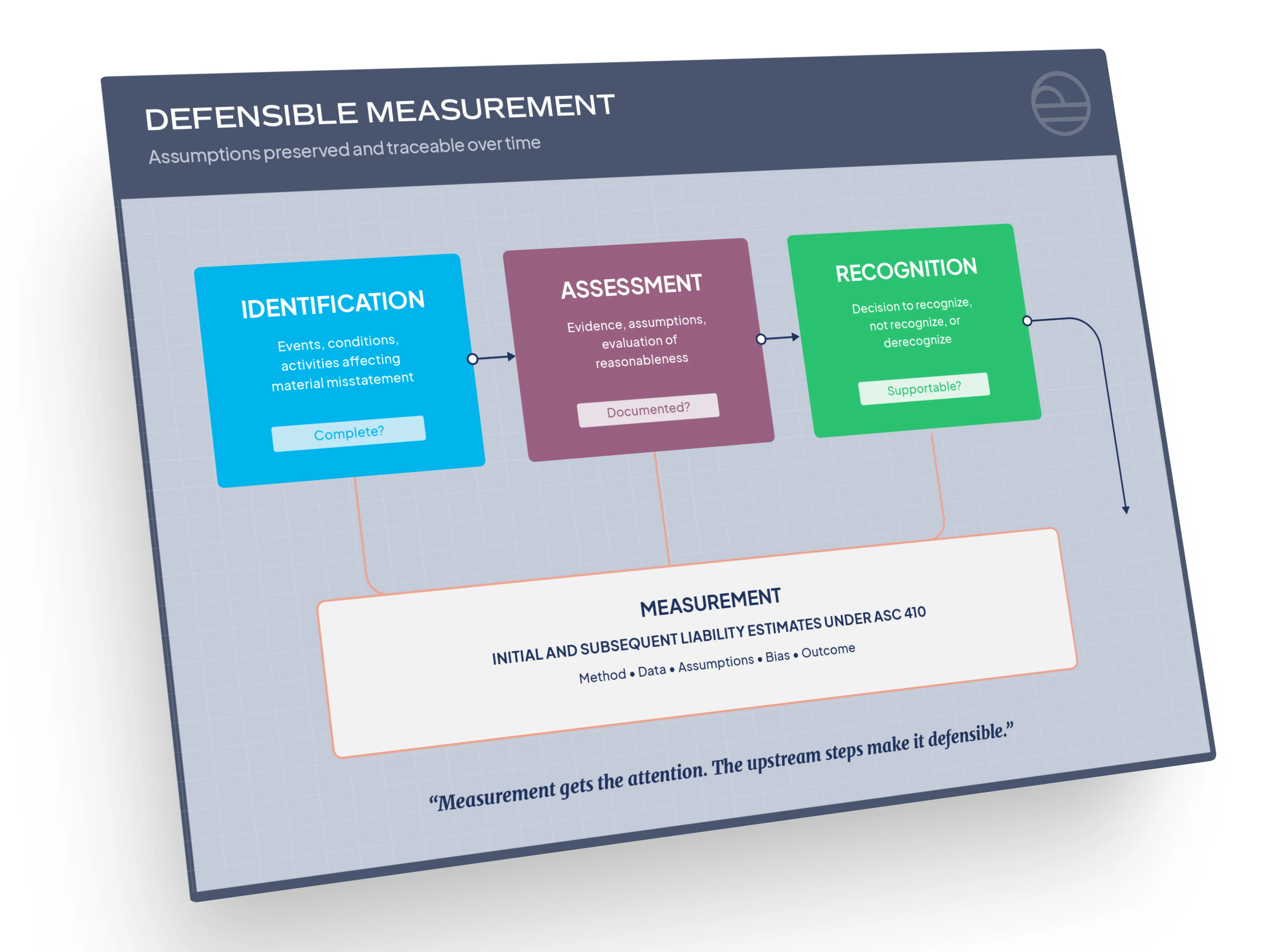

Defensible measurement depends on a sequence of upstream decisions that precede the calculation of a liability estimate. These steps form the foundation of measurement and must be governed with the same rigor as the resulting numbers:

- Identification: Events, conditions, and activities that may give rise to Environmental Obligations and affect the risk of material misstatement.

- Assessment: Relevant evidence and assumptions for identified obligations, evaluated for completeness and reasonableness.

- Recognition: A documented and supportable decision to recognize, not recognize, or derecognize an obligation in accordance with GAAP recognition and materiality criteria.

- Measurement: Liability estimates prepared in accordance with ASC 410 requirements for Asset Retirement Obligations and Environmental Remediation Obligations, including initial and subsequent measurements over time.

These steps are not optional. PCAOB standards require auditors to evaluate whether Environmental Obligations exist, whether they are complete, and whether recognition and measurement are supported by appropriate evidence. Measurement follows recognition. ASC 410 governs how liabilities are measured. PCAOB AS 2501 defines how auditors evaluate whether methods conform to GAAP, data is complete and accurate, assumptions are reasonable, and estimates are supportable.

Measurement receives the attention. Identification, assessment, and recognition determine whether that measurement is defensible over time.

The Structural Breakdown

The governing mandate is clear. Execution of that mandate is not.

Most organizations lack the infrastructure to govern identification through measurement as a unified, controlled process. Instead, these steps are fragmented across functions, systems, and time. Each step is owned and managed in isolation. The result is a governance model that exists on paper but fails in practice.

Identification is incomplete or informal. Assessment is undocumented. Environmental Obligations enter the inventory late, or not at all, because no governed process exists to surface them consistently. When obligations are identified, supporting evidence and assumptions are rarely preserved. Reasonableness is implied rather than demonstrated. Auditors ask questions that require reconstruction rather than retrieval.

Recognition decisions are implicit rather than documented. Decisions to recognize, not recognize, or derecognize Environmental Obligations are among the most consequential judgments in Environmental Obligation Management. Yet many organizations cannot produce a clear record of when those decisions were made, who made them, what evidence supported them, or how they aligned with GAAP recognition criteria.

Measurement inherits these upstream gaps. By the time a liability reaches measurement, it carries the accumulated weaknesses of the steps that preceded it. Incomplete identification results in missing obligations. Undocumented assessment leaves assumptions unverified. Accounting inputs such as discounting, accretion, and depreciation are disconnected from the underlying obligation facts. Measurement may appear precise, but precision built on an incomplete foundation does not equal accuracy.

EXPLORE ENFOS TODAY

The Strategic Consequences

Weaknesses in measurement do not remain hidden. They are exposed under scrutiny, when the cost of correction is highest.

Audit Readiness Erodes: Auditors evaluate the full lifecycle of Environmental Obligation processes, not just ending balances. When upstream steps are undocumented, audit procedures expand and become reconstruction exercises. Review cycles extend, costs increase, and the risk of audit findings compounds.

Financial Statement Integrity Is Compromised: Environmental Obligations may be understated because obligations were never identified, indefensible because recognition decisions cannot be traced, or misstated because assumptions were never documented or tested. Balances reach the financial statements, but the underlying support cannot withstand scrutiny.

Executive Decision-Making Is Weakened: Executives and boards rely on measured Environmental Obligations to evaluate exposure, risk, and financial position. When measurement lacks traceability, confidence in reported liabilities erodes. Transactions and other enterprise-level decisions surface gaps that steady-state operations concealed.

Measurement failures do not announce themselves early. They surface when defensibility matters most.

Category Implication

Defensible measurement of Environmental Obligations requires assumptions that are preserved, governed, and traceable over time.

Environmental Obligation Management defines the discipline for governing identification, assessment, recognition, and measurement of Environmental Obligations within a controlled system of record. That system of record must preserve assumptions, supporting evidence, and decision history across reporting periods so that measured liabilities remain defensible under audit and scrutiny.

Without governed measurement, financial reporting integrity degrades over time. Environmental Obligation Management exists to ensure that Environmental Obligations are measured completely, measured correctly, and supported for as long as they remain on the balance sheet.