The Governing Mandate

Environmental Obligations cannot be governed without a complete and structured inventory. Identification is the first control point in the lifecycle of Asset Retirement Obligations (ARO) and Environmental Remediation Obligations (ERO). Accounting standards require that organizations identify Obligations completely and evaluate them consistently before recognition, measurement, or disclosure can occur. An obligation that is not inventoried cannot be governed, measured, or defended.

This requirement is embedded directly in financial reporting standards. ASC 410-20 and ASC 410-30 require organizations to identify and assess Obligations at the asset or site level before determining recognition, materiality, and measurement treatment. Auditors evaluate whether management has established processes to identify Obligations completely and whether those processes operate consistently over time. Regulators and investors expect that recognized liabilities reflect the full scope of known and reasonably estimable Environmental Obligations, with transparent disclosure of additional exposures.

A complete inventory is not optional or administrative. It is the foundation of financial accuracy, audit readiness, and enterprise governance. Without it, every downstream process is compromised.

The Structural Breakdown

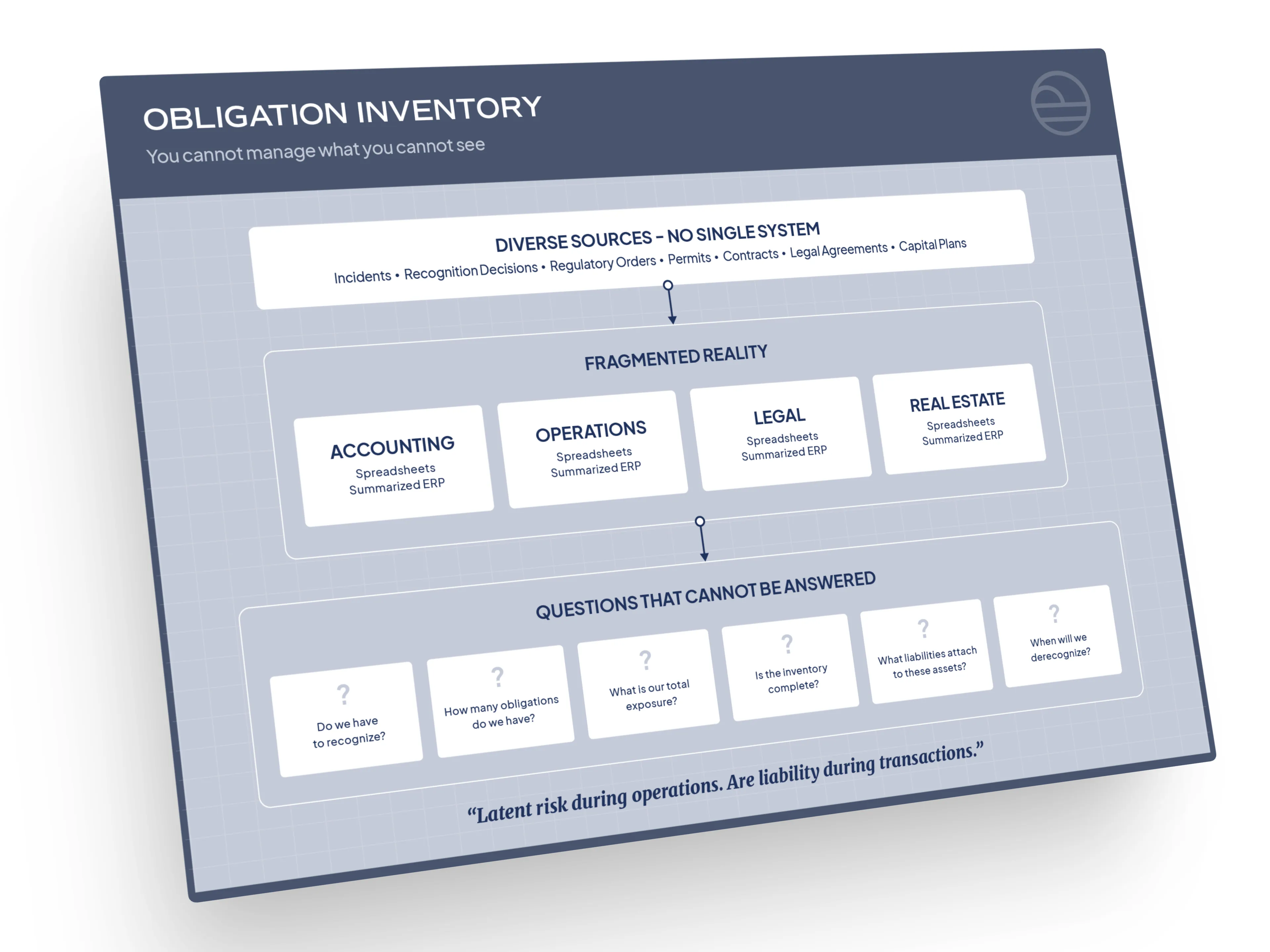

In practice, most enterprises do not maintain a complete, structured, and governed inventory of Environmental Obligations. The breakdown is systemic and predictable.

Obligations originate across diverse sources. Regulatory orders, permits, environmental assessments, incident reports, contractual commitments, Asset Retirement plans, legal agreements, and capital projects all generate potential ARO and ERO exposure. These sources span geographies, business units, legal entities, and external partners. No single function owns the full intake process, and no single system consolidates Obligations into an authoritative record.

Inventories, where they exist, are fragmented. Accounting teams maintain summarized lists tied to financial models. Operations teams track sites and projects in spreadsheets or point solutions focused on execution. Legal and real estate teams maintain separate records tied to transactions or property ownership. These inventories differ in structure, level of detail, and purpose. They are not reconciled continuously and are rarely governed through formal controls.

Completeness cannot be verified. Legacy Obligations fade as institutional knowledge turns over. New Obligations emerge as site conditions change or regulations evolve without being consistently captured. Watch-list Obligations that may require future recognition are inconsistently tracked or lost entirely. Organizations cannot assert with confidence that their inventory reflects the full population of Obligations, and neither can their auditors.

The result is an inventory that exists in fragments but does not function as a system of record.

EXPLORE ENFOS TODAY

The Strategic Consequences

An incomplete or inconsistent inventory creates enterprise-level risk that compounds over time.

Governance Risk: An incomplete or unstructured Environmental Obligation inventory is not merely an operational inconvenience. It is a source of material governance risk. Incomplete obligation tracking often remains latent during steady-state operations but becomes acute during audits, transactions, and regulatory scrutiny, when counterparties, auditors, and counsel examine what the organization never systematically captured.

Financial Statement and Disclosure Risk: Financial statements may understate Environmental Obligations when Obligations are missing from the inventory entirely. Reserves may be misstated when obligation attributes are inconsistent, outdated, or incomplete. Audit responses devolve into reconstruction exercises rather than controlled retrieval of data. Strategic decisions, including acquisitions, divestitures, and portfolio changes, proceed without full visibility into Environmental Obligations that can alter deal economics or delay execution.

Executive and Board Oversight Risk: Executives and boards cannot exercise effective oversight over Environmental Obligations they do not know exist or cannot trace to a reliable inventory. Reporting and disclosure controls weaken when underlying obligation data is incomplete, leaving the organization vulnerable to surprises that a proper inventory would have surfaced years earlier.

An inventory gap is rarely visible in isolation. It surfaces under scrutiny, when correction is most costly.

Category Implication

Environmental Obligation Management must begin with a complete, structured inventory.

This requires a governed system of record that consolidates ARO and ERO at the asset and site level, preserves critical attributes, and supports continuous identification as conditions evolve. The inventory must be auditable, extensible, and maintained as a living financial control, not a static list.

Without a structured inventory, governance, measurement, execution, and reporting cannot scale. Environmental Obligation Management establishes the inventory as the foundation on which all downstream control depends.