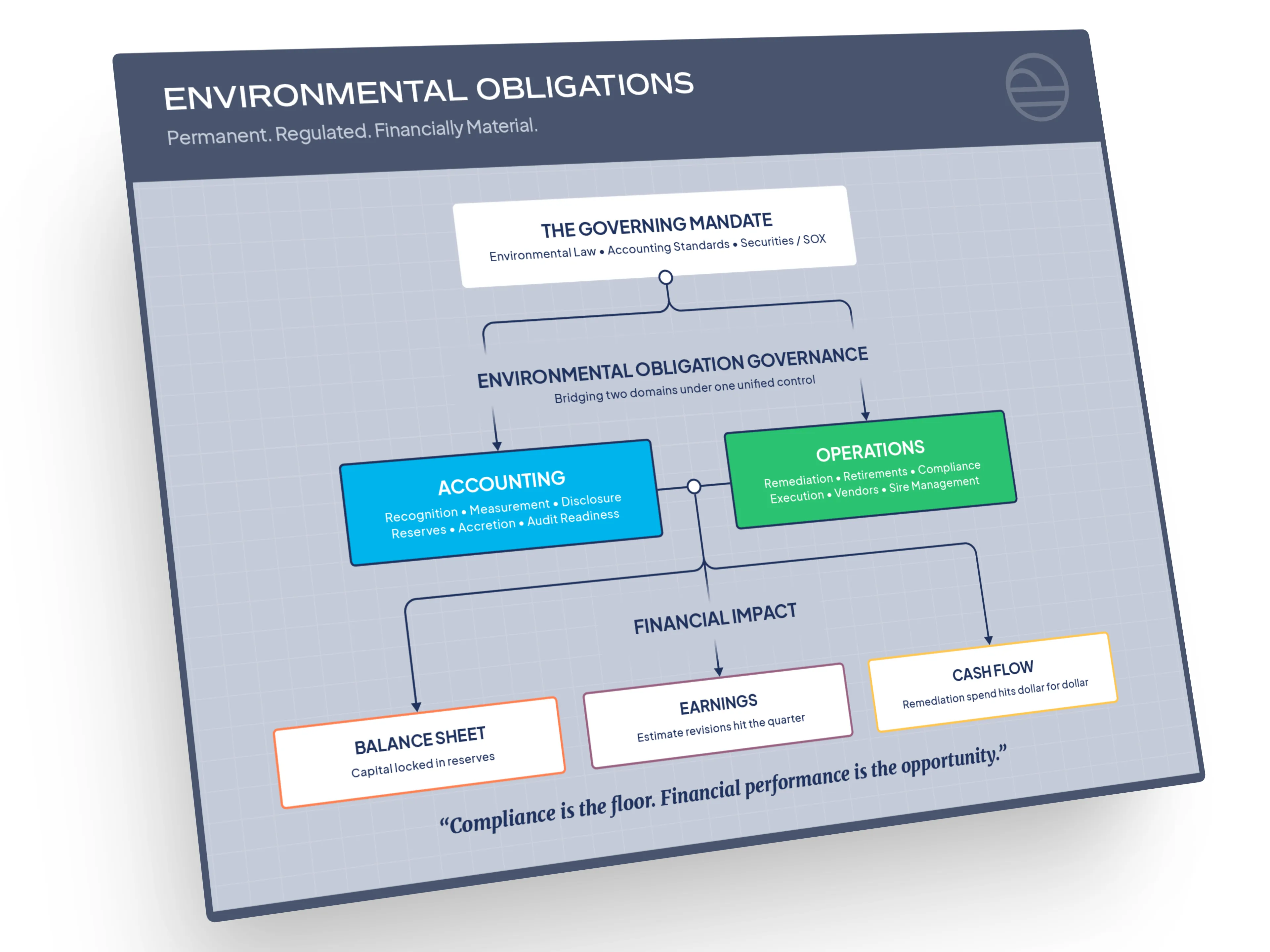

The Governing Mandate

Every organization that operates physical infrastructure carries Environmental Obligations. These obligations arise from environmental law, contractual commitments, and regulatory requirements tied to the operation, retirement, and remediation of long-lived assets. They often originate when an asset is placed into service and persist until the obligation is fully satisfied through remediation, closure, or retirement activities. Environmental Obligations are not discretionary, temporary, or episodic. They are permanent features of the enterprise balance sheet.

This mandate is enforced by a layered regulatory and financial reporting framework. Environmental laws at the federal, state, and local levels require organizations to remediate contamination and can impose legally enforceable asset retirement or restoration duties. Securities regulations require public companies to disclose material environmental exposures accurately and consistently. Accounting standards, including ASC 410-20 for Asset Retirement Obligations (ARO) and ASC 410-30 for Environmental Remediation Obligations (ERO), prescribe how these obligations must be identified, measured, remeasured, and disclosed over time. Sarbanes-Oxley (SOX) elevates these requirements to the executive level by requiring CEOs and CFOs to personally certify financial statements.

The result is a non-negotiable mandate. Environmental Obligations must be governed as a financial discipline over decades, not managed as isolated compliance tasks or operational projects. Failure to do so exposes the enterprise to regulatory enforcement, financial restatement risk, reputational damage, and erosion of investor confidence.

The scale of this exposure is significant. Asset-intensive enterprises routinely carry Environmental Obligations measured in hundreds of millions or billions of dollars. These liabilities span large portfolios of assets and sites, involve long planning horizons, and require continuous reassessment as conditions, regulations, and execution progress change. By any reasonable standard, Environmental Obligations are financially material.

The Structural Breakdown

Despite their permanence and financial materiality, most organizations manage Environmental Obligations with processes and systems that are not designed to withstand sustained complexity or scrutiny. The breakdown is structural, not incidental.

Environmental Obligation data is fragmented across spreadsheets, point solutions, and function-specific tools. Finance teams maintain summarized liability models focused on financial reporting. Operations teams manage scientific data, remediation plans, and execution activity in separate systems or files. Legal and real estate teams track obligations through their own documentation. These systems are loosely connected, if at all, and rarely governed as a single source of truth.

Assumptions underlying recognition and measurement drift over time. Version control is manual. Historical decisions are overwritten rather than preserved. The linkage between operational reality and reported financial balances weakens as portfolios grow, personnel change, and obligations persist across decades. Governance exists in policy documents and organizational charts, but not in the systems that actually produce the numbers.

This fragmentation creates a persistent governance gap. Environmental Obligations sit at the intersection of finance, science, and operations, yet no unified framework exists to control the full lifecycle from identification through execution and settlement. The result is a collection of ad hoc workflows that function during steady-state periods but fail under scale, turnover, audit, or transaction pressure.

EXPLORE ENFOS TODAY

The Strategic Consequences

When Environmental Obligations are not governed as a permanent financial category, enterprise risk compounds over time.

Financial integrity erodes as liability estimates diverge from execution reality. Reserves may be overstated, trapping capital on the balance sheet, or understated, creating future earnings volatility. Period-to-period revisions become harder to explain and defend as assumptions and decision history disappear. CFOs and Controllers face increasing difficulty certifying balances with confidence.

Audit and regulatory exposure intensifies. Auditors evaluate not only ending balances but the controls and judgments that produced them. When documentation, traceability, and historical support are fragmented, audit cycles lengthen, costs rise, and findings become more likely. Regulatory inquiries expose the difference between stated governance and actual practice.

Strategic decision-making suffers. Capital allocation, forecasting, and M&A diligence depend on accurate, governed liability data. When Environmental Obligations are poorly structured, executives and boards make decisions without a clear view of long-term exposure. Enterprise value becomes vulnerable to risks that were known but not systematically governed.

Environmental Obligations do not diminish with time or attention. They persist, evolve, and accumulate. Managing them through improvised tools and fragmented ownership is not a viable long-term strategy.

Category Implication

The market requires a distinct enterprise discipline: Environmental Obligation Management.

Environmental Obligation Management is the governance of permanent, regulated, and financially material Environmental Obligations through a single, controlled system of record that integrates financial, scientific, and operational data. It enables organizations to identify, measure, remeasure, and report obligations defensibly over time while maintaining audit readiness, transparency, and accountability at scale.

This is not an operational enhancement. It is a financial necessity.